Like the notion of technical debt, the concept of management debt relates to the leadership issues that prevent a successful Agile transformation. This article from Agile transformation expert Sriram Rajagopalan discusses the types of waste that can be eliminated using a Kanban approach and the role of management debt in perpetuating wasteful practices.

Author: Sriram Rajagopalan, http://agilesriram.blogspot.com/

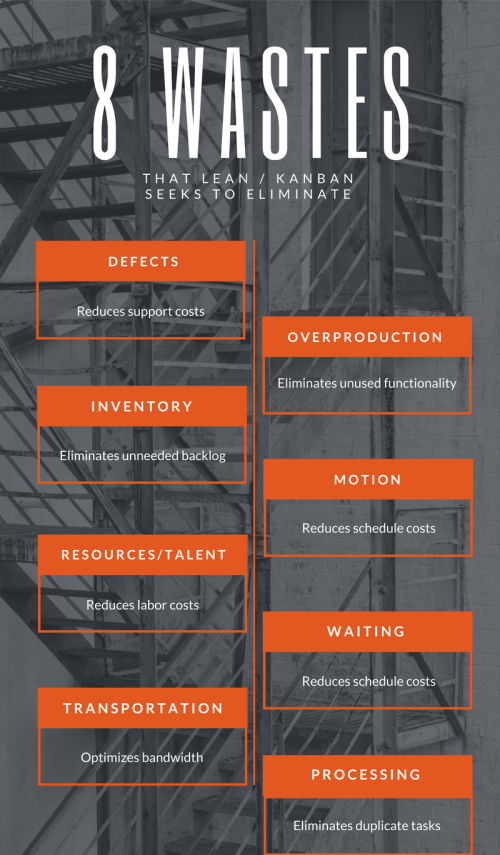

The principles of lean have always focused on maximizing the value delivery. In fact, the Japanese term Muda (Arnheiter & Maleyeff, 2005) refers to the seven different types of wastes that one should remove. Expanding on the standard seven types of waste in Kanban, practitioners have added the non-utilization of talents introducing the mnemonic or memory aid, DOWNTIME, to capture these eight types of waste an organization or project should closely monitor to increase efficiency. These eight type of wastes are:

* Defects

* Over-production

* Waiting

* Non-utilized resources and talent

* Transportation

* Inventory

* Motion

* Excess processing

Often, these eight principles are considered an academic exercise and practitioners have lost connection with these principles. Unless these principles are related in terms of the management language, money, these principles don’t gain the limelight. In this article, I would like to synthesize some of these principles in terms of two types of costs as follows that relate to the cost of poor quality. When these two costs are not managed appropriately, they add management debt to the project.

Cost of Non-Delivery

This principle refers to the “…measure of the costs associated with preventing, testing for, or correcting defective items,” according to Carr (1992, p. 72). The cost of poor quality comes from both the internal and external failure costs where poor quality costs are associated with rework, redesign, retesting, failure in or shortage of specifications in requirements, bugs arising from poor development practices or myopic understanding of or inaccuracies in requirements or design, or unplanned delays in monitoring the dependencies.

All these relate to elements mentioned in the DOWNTIME factors and could lead delivered work that is still not production ready unacceptable for customers. Say, if any of the above factors contributed to a schedule slip of 10% on a project that cost $100,000. At a minimum level, this slip means $10,000 (10% of $100,000) is now an additional cost to the project that could have been effectively controlled.

Cost of Non-Conformance

Non-conformance means the rules of engagement for a specific development or management methodology are not completely adhered. For example, not following the integrated change control mechanism to use a tool that is not approved by the organizational policies, not adequately preparing for the specific meetings increasing the cost of a meeting, taking missteps that lead to the escaped defects increasing customer’s bad will, or over-engineering a feature beyond the fitness for use.

When these things happen, it often involves more time spent in corrective actions introducing increased testing, executing recalls and incurring expenses on the performing company’s time and money, or attempts at various levels to restore customer satisfaction. The cost of non-conformance retraces its roots to the cost of quality examples on lack of adherence to existing policies.

Summary

Therefore, middle management focusing on delivering products or projects, whether they operate through traditional or agile approaches, should evaluate the cost of non-delivery and cost of non-conformance to ensure that all these waste producing efforts are eliminated. Management is obligated to monitor these patterns that lead to the management debt similar to the technical debt. Only when this management debt is controlled, the concept of efficiency grows with the seeds of cost of good quality.

References

* Arnheiter, E.D. and Maleyeff, J. (2005) ‘The integration of lean management and Six Sigma’, The TQM Magazine, 17(1), pp. 5–18.

* Carr, L. P. (1992, Summer). Applying cost of quality to a service business. Sloan Management Review, 33(4), 72.

Further Reading

If you are interesting in learning more about Management Debt and how it can impede the adoption of Agile Methodologies, read Agile Transformation Failure – Understanding Management Debt.

About the author

Dr. Sriram Rajagopalan is the Vice President of Proposition Delivery with Aptus Health. He holds a BA in Electronics and Communication Engineering from the University of Madras in India. He has also a MS in Computer Engineering from Wayne State University, Michigan, and MBA in Management from Concordia University, Wisconsin. His PhD is in Organization and Management from Capella University, Minnesota. Dr. Rajagopalan has professional certifications in PMP, PMI-ACP, PMI-SP, PMI-RMP, CSP, CSPO, CSD, CSM, ACC, IT Project+, SCM, SCPO, SCD, SAMC, SCT, and CSOXP. This article was originally published on https://www.inflectra.com/Ideas/Entry/432.aspx and is reproduced with permission from Inflectra.